Central Bank of Ireland

| Headquarters | |

|---|---|

| Established | 1 February 1943 |

| Ownership | 100% state ownership[1] |

| Governor | Gabriel Makhlouf ( since September 2019) |

| Central bank of | Ireland |

| Reserves | 740 million USD[1] |

| Preceded by | Currency Commission (currency control) Bank of Ireland (Government's banker)1 |

| Succeeded by | European Central Bank (1999)2 |

| Website | centralbank |

| 1 Even after establishment of the Central Bank, the Bank of Ireland remained the government's banker until 1 January 1972. 2 The Central Bank of Ireland still exists but many functions have been taken over by the ECB. | |

The Central Bank of Ireland (Irish: Banc Ceannais na hÉireann) is Ireland's central bank, and as such part of the European System of Central Banks (ESCB). It is the country's financial services regulator for most categories of financial firms. It was the issuer of Irish pound banknotes and coinage until the introduction of the Euro currency, and now provides this service for the European Central Bank.

The Central Bank of Ireland was founded on 1 February 1943, and since 1 January 1972 has been the banker of the Government of Ireland in accordance with the Central Bank Act 1971,[2] which can be seen in legislative terms as completing the long transition from a currency board to a fully functional central bank.[3]

Its head office, the Central Bank of Ireland building, was located on Dame Street, Dublin from 1979 until 2017.[4] Its offices at Iveagh Court and College Green also closed down at the same time. Since March 2017, its headquarters are located on North Wall Quay, where the public may exchange non-current Irish coinage and currency (both pre- and post-decimalization) for Euros, as well as high value Euro banknotes and "mutilated" currency.[5] It also operates from premises at nearby Spencer Dock. The Currency Centre (Irish Mint) at Sandyford is the currency manufacture, warehouse and distribution site of the bank.[6]

The Central Bank's reputation was damaged in the Irish financial crisis. While the Bank has taken actions to address some of the main criticisms (e.g. mortgage lending controls, and the new modified gross national income metric), there is evidence other issues remain (e.g. commercial property bubbles, and light-touch regulation), and that new controls, such as mortgage limits, are being circumvented by Irish banks and the Irish State.

History[]

From Currency Commission to Central Bank (1920–1942)[]

On the independence of the Irish Free State in 1922, the new state's trade was overwhelmingly with the United Kingdom (98% of Irish exports and 80% of imports in 1924),[citation needed] so the introduction of an independent currency was a low priority. British banknotes (British Treasury notes, Bank of England notes), and notes issued by Irish trading banks circulated (but only the first were legal tender) and British coins remained in circulation.

Under the terms of the Coinage Act 1926, the Finance Minister was authorised to issue coins of silver, nickel, and bronze of the same denominations as the British coins already in circulation – however, the Irish silver coins were to contain 75% silver as compared to the 50% silver coins issued by Britain at the time. These coins entered circulation on 12 December 1928.

Under the terms of the Currency Act 1927, a new unit of currency, the Saorstát Pound (Free State Pound) was created, which was to be maintained at parity with the British Pound Sterling by a Currency Commission which would keep British government securities, Pounds Sterling cash, and gold to keep a 1–1 relationship.

From 1928 to 1979, the U.K. and Ireland were in a de-facto currency union.

Foundation of the Central Bank to decimalization (1942–1971)[]

The Central Bank Act 1942 which came into effect on 1 February 1943 renamed the Currency Commission the Central Bank of Ireland, although the organisation did not at that time acquire many of the characteristics of a central bank:

- it was not given custody of the cash reserves of the commercial banks

- it had no statutory power to restrict credit, though it could promote it

- the Bank of Ireland remained the government's banker

- the conditions for influencing credit through open-market operations did not yet exist

- Ireland's external monetary reserves were largely held as external assets of the commercial banks

The mid-1960s saw the Bank take over the normal day-to-day operations of exchange control from the Department of Finance. The Central Bank broadened its activities over the decades, but it remained in effect a currency board until the 1970s. Economist Patrick Honohan evaluates the success of the movement from a currency board to the central bank as follows: 'in contrast to many other post-colonial cases, (the currency board's) demise was not followed by a rapid depreciation and slide into semi-permanent high inflation and lack of convertibility.[7]

Such was the proliferation of small industrial banks and hire purchase firms in the late 1960s, the 1971 Central Bank Act introduced significantly enhanced authorisation and supervision standards. In the inevitable consolidation in the marketplace, in 1976 a liquidator was appointed to Irish Trust Bank Ltd after Central Bank investigations and in 1982 Merchant Banking Ltd also collapsed.

Decimalization to European integration (1971–1978)[]

The 1970s was a decade of change, which began with the decimalisation of the currency which came into effect on 15 February 1971, when the decimal coinage was released into circulation (although 5p, 10p, and 50p coins were released a few years earlier, as they had exact equivalents in old currency units). Decimalisation would have provided an ideal opportunity to break the link with the Pound Sterling, but there was not much demand for this at that time. In 1972 however, the Bretton Woods system of fixed exchange rates broke down, and in the wake of the 1973 oil crisis inflation in Britain increased dramatically, and economic theory would suggest that a smaller economy whose currency is pegged to a larger one will suffer the larger economy's inflation rate. At the same time moves to create a money market in Dublin and the transfer in 1968 of the commercial banks' Pound Sterling assets to the Central Bank made it possible to contemplate a break in the link. In the mid to late 1970s, opinion within the bank was moving toward breaking the link with the Pound Sterling and devaluing the Irish currency in order to limit inflationary effects from abroad.

The EMS and movement toward a single currency[]

This section does not cite any sources. (December 2018) |

At this time, however, an alternative option became available. In April 1978, the European Council meeting in Copenhagen decided to create a "zone of monetary stability" in Europe, and European Economic Community institutions were invited to consider how to create such a zone. At the following Council meeting in Bremen, Germany in June 1978 the basic features of the European Monetary System were outlined, including the creation of the ECU – European Currency Unit, a basket of the Community's currencies used to determine exchange rates, and the forerunner of the Euro.

The Irish government had to decide whether or not to participate in the EMS. If the EMS had included all the European Economic Community's currencies, it would have provided stability for 75% of Ireland's external trade, but Britain, which still accounted for 50% of Ireland's external trade, decided to stay out of the EMS. Despite this, on 15 December 1978, it was announced that Ireland would participate in the EMS. Countries were given the option of either a 2.25% or 6% margin of fluctuation within the EMS' Exchange Rate Mechanism (ERM), and Ireland took the narrower margin. The EMS started on 13 March 1979, and towards the end of the month the Pound Sterling started to gain in value against the EMS currencies because of rising oil prices, and by 30 March the Pound Sterling breached the upper fluctuation band limit of the Belgian franc and the Irish currency could no longer track the Pound Sterling. After over 50 years, the parity of the Irish and British currencies was broken, and the Irish currency became known as the Irish pound (or Punt in the Irish language).

The initial experience of the EMS was disappointing. It had been expected that the Irish Pound would appreciate in value against the Pound Sterling, and hence reduce inflation in Ireland, but in practice, Sterling appreciated considerably in value thanks to its status as a petrocurrency and to the tight monetary policies of the new British government of Margaret Thatcher. By late 1980 the Irish Pound had fallen in value to less than 80 British pence, and Irish inflation was higher than British. Economic policy in Ireland was inconsistent with a "hard currency" policy, and the Irish Pound also failed to hold its value against the central rate of the Deutschmark, although it did appreciate in value against some of the other EMS currencies.

Eventually, the EMS settled down (notwithstanding a crisis in 1992 when the Irish Pound was devalued by 10%), and Irish inflation was the same or lower than Britain's inflation rate from 1987 onwards.

Towards the Euro[]

The idea of a single European currency goes back to the Schumann Plan of 1950. The first blueprint for how to go about implementing the currency, the Werner Report of 1970 was not proceeded with, but the ultimate aim was always kept in mind. The Delors Report endorsed by the Madrid Summit of June 1989 envisaged a three-stage process to monetary union, and this was given legal authority by the Maastricht Treaty of 1992 (enacted into Irish law as the Eleventh Amendment to the Constitution of Ireland by 70% of those voting in a referendum on 18 June 1992). This envisaged the start of monetary union on 1 January 1999 and the introduction of notes and coins on 1 January 2002.

The Central Bank began production of euro coins in September 1999 in the Currency Centre (Irish Mint) in Sandyford, producing over a billion coins, weighing about 5,000 tons, with a value of €230 million before the introduction into circulation of the euro coins in January 2002. Production of euro banknotes began in June 2000, with 300 million notes worth €4 billion being produced in denominations of 5, 10, 20, 50, and 100 euros. Euro banknotes produced for the Central Bank are identified by having the serial number beginning with the letter T. The Bank did not initially issue €200 or €500 notes but has since begun to do so.[8]

Domestic banking crisis[]

The Central Bank noted in November 2005 that an overvaluation existed of 40% to 60% in the Irish residential property market. Minutes of a meeting with the OECD indicated that while the Central Bank agreed that Irish property was overvalued it was fearful of precipitating a crash by "putting a number on it". Senior Allied Irish Bank officials expressed concerns in 2006 that Central Bank stress tests were "not stressful enough".[9] The management ignored warnings from its own financial stability unit, according to one former staff member, whose evidence to the parliamentary inquiry was questioned by a number of other staff members,[10] and from the Economic and Social Research Institute about the scale of bank loans to property speculators and developers[11] leading to key information being suppressed. It was reported that it sought to gag a prominent economist from talking about the fragile state of the nation's banks in relation the Irish branch of Northern Rock.[12] The Central Bank "watered down" economic warnings about the property bubble in the run-up to the crash, blocked internal communication reaching board level due to the political interests, and "rigorously" concealed data from the relevant external supervisors on the large exposures of Irish banks to individual developers.[13][14]

In November 2007, they stated: "The Irish banking system continues to be well-placed to withstand adverse economic and sectoral developments in the short to medium term. The underlying fundamentals of the residential market continue to appear strong and the current trend in monthly price developments does not imply a sharp correction. The central scenario, therefore, is for a soft landing."[15]

After the bubble burst, Irish banks faced mounting losses which exposed them to a collapse of confidence following the Lehman Brothers bankruptcy in September 2008; they then suffered acute liquidity pressures which had to be met by Central Bank support, including emergency lending. Management abuses were also revealed at Anglo Irish Bank, which had to be nationalised in January 2009.

The Central Bank annual report, published three months before the Irish State unconditionally guaranteed the deposits of Irish-owned banks, said: "The banks have negligible exposure to the sub-prime sector and they remain relatively healthy by the standard measures of capital, profitability and asset quality. This has been confirmed by the stress testing exercises we have carried out with the banks".[16][17]

The next annual report had little to say about how and why the Irish banking system collapsed.[18] Although there were four Central Bank directors on the board of the Financial Regulator, the Central Bank maintained it had no powers to intervene in the market. Yet, the Central Bank had the power to issue directives to the Financial Regulator if it thought it was conducting its business in a way that was contrary to overall Central Bank policy aims. None were issued.[19][20]

The regulator's processes and reports, and the findings of external scrutineers, any of which should have raised red flags, failed to do so. As a result, they did not see the enormity of the risks being taken by the banks and the calamity that was to overwhelm them.[21]

The European Commission in a November 2010 review of the financial crisis said: "Some national supervisory authorities failed dramatically. We know that in Ireland there was almost no supervision of the large banks."[22] Two months later, the President of the EU Commission in an angry exchange in the European Parliament, with a vehemence that shocked his audience, said that "the problems of Ireland were created by the irresponsible financial behaviour of some Irish institutions, and by the lack of supervision in the Irish market."[23]

Separation of regulation – The Financial Regulator[]

In 2003 a new separate division of the Central Bank, with its own Chairman, Chief Executive, and board, was established as the Irish Financial Services Regulatory Authority. This was a compromise between those who favoured a fully independent regulator and those who believed the Central Bank should maintain full control of regulation of the financial services industry. This division of the Bank authorised and regulated all financial institutions (including insurance undertakings, collective investment funds and credit unions) in Ireland.[24][25] The "Central Bank of Ireland" was formally renamed Central Bank and Financial Services Authority of Ireland (CBFSAI). (There was no entity named "Financial Services Authority of Ireland".)

Under the 2003 arrangements, the Central Bank provided the Financial Regulator with services. The Regulator's industry panel, which provided the Regulator with feedback on its charges and policies said in April 2007 that they had ‘‘major concerns with the quality and cost of the services’’ provided to the Regulator by the Central Bank.[26]

The operations of the Financial Regulator were severely criticised in a report marked "strictly confidential and not for publication", as being poor value for money. The report stated that there were too few specialist staff, compared with its peers.[27] There were also serious shortcomings in the crucial supervisory area.[28][29] and the report was particularly critical of the regulator's senior management structure, concluding that a clear management and oversight framework, which ensures that issues are escalated through the organisation, was "not fully in place".[30]

Former Taoiseach Bertie Ahern, said that his decision in 2001 to create a new financial regulator was one of the main reasons for the collapse of the Irish banking sector and "if I had a chance again I wouldn't do it".[31] Ahern said: "The banks were irresponsible. But the Central Bank and the Financial Regulator seemed happy. They were never into us saying – ever – 'Listen, we must put legislation and control on the banks'. That never happened."[32]

In April 2010, the new Financial Regulator, outlined his shock at the poor level of financial regulation he discovered when he started his job the previous January and "it is clear to me we need to undertake a fundamental overhaul of the regulatory model for financial services in Ireland."[33] He also said that there was a "critical absence of intellectual firepower within his staff".[34]

Following the banking collapse of 2008 and 2009, the Government[35] re-unified the organisation under a Central Bank of Ireland Commission to replace the board structures of the Central Bank and the Financial Services Regulatory Authority which became effective on 1 October 2010. The name "Central Bank of Ireland" was restored. A July 2009 editorial in the Sunday Business Post said "returning the key powers of regulation to the Central Bank will be useless unless there is a fundamental change in the culture of the organisation. This does not require a complete change of personnel, but a change of key personnel."[36] There can be no denying that the spinning off of the Financial Regulator from the functions of the Central Bank in 2003, was an outright failure.[37][38]

Post crisis reforms[]

On 4 November 2014 the European Central Bank formally took supervisory control over the biggest banks in Europe, including those in Ireland. While banking supervision staff in the Central Bank of Ireland remained, a pan-European approach to how banks were supervised was introduced, the Single Supervisory Mechanism.[39]

Subsequent to the parliamentary inquiry into the domestic banking crisis the organization said that the actions taken by the Central Bank combined with legislative reform and an overhaul of international regulation have enabled the organization to deliver effective supervision and financial stability measures since the crisis. Governor Philip Lane said, "The report describes a failure to identify risks to financial stability and recognizes the lack of an overall European framework to deal with the financial and fiscal crises. Many of the issues identified by the Inquiry relating to the Central Bank have been substantially addressed or continue to be addressed through measures including significant institutional reform, additional powers, the promotion of a culture of challenge and the implementation of the model of assertive risk-based supervision underpinned by a credible threat of enforcement."[citation needed]

In early 2015 the Central Bank introduced macro-prudential mortgage regulations to increase the resilience of the banking and household sectors to the property market and to reduce the risk of bank credit and house price spirals from developing in the future.[40] These measures are to be reviewed annually, with the first report published in November 2016.[41]

In response to the July 2016 leprechaun economics affair, on the request of the Central Statistics Office ("CSO"), the Governor of the Central Bank chaired a cross economic steering group (Economic Statistics Review Group, or "ESRG") including the IFAC, ESRI, NTMA, leading academics and the Department of Finance, to recommend new economic statistics to the CSO, that would better represent the Irish economy (given the escalating distortions in GDP and GNP).[42] The result was the introduction of "modified GNI" (or GNI*). Report Site of the ESRG.[43][44] 2016 Modified GNI* is 70% of 2016 GDP (or 2016 GDP is 143% of 2016 GNI*).

Historical archives and data[]

The Central Bank opened its archives to the public in 2017 operating a 30 year rule for the release of records.[45] The archives can be accessed by means of the Banks online finding aid and consulted in the Bank's North Wall Quay premises in Dublin.[46]

The bank releases data on the changing wealth of Irish households.[47]

Responsibilities[]

The Central Bank of Ireland's mandate calls on it to contribute to the well being of the people of Ireland and more widely in Europe by performing statutory responsibilities which cover a wide range, including :

- price stability;

- financial stability;

- consumer protection;

- supervision and enforcement;

- regulatory policy development;

- payment, settlement and currency systems operations and oversight;

- the provision of economic advice and financial statistics; and

- the recovery and resolution of distressed financial services firms.

Governors[]

The Governor of the Bank is appointed by the President of Ireland on the constitutional advice of the Government of Ireland.

| Name (Birth–Death) |

Term of office |

|---|---|

| Joseph Brennan (1887–1963) |

1943–1953 |

(1890–1974) |

1953–1960 |

| Maurice Moynihan (1902–1999) |

1960–1969 |

| T. K. Whitaker (1916–2017) |

1969–1976 |

(1917–2008) |

1976–1981 |

(1921–2015) |

1981–1987 |

(1932–2009) |

1987–1994 |

| Maurice O'Connell[48] (1936–2019) |

1994–2002 |

(1945 – ) |

2002–2009 |

| Patrick Honohan (1949 – ) |

2009–2015 |

| Philip R. Lane (1969 – ) |

2015–2019 |

| Gabriel Makhlouf (1960 – )[49] |

2019–Present |

Criticisms[]

This article may primarily relate to a different subject, or place undue weight on a particular aspect rather than the subject as a whole. (July 2019) |

Recurrent criticisms were made both before and after the Irish banking crisis, of the Central Bank of Ireland.[51] As seen in the Irish banking crisis, when global markets are stressed, several of these issues can occur simultaneously (i.e. they are not independent risks), to amplify the seriousness of the situation. While the pre-crisis Central Bank of Ireland was judged to fail on all these criticisms,[51] the Irish State had the financial resources to bail out the Irish banking system (Ireland was almost debt-free before the crisis).[52][53] Post the 2011–bailout, the Irish State has a debt-to-GNI* ratio of over 100%,[54][55] and will not be able to withstand such a material failing by the Central Bank of Ireland again. A recurrence would place the Irish banking system, and the Irish State, into creditor restructuring.

Green jersey agenda[]

In 2016, several Irish bank CEOs testified to being asked by senior officials of the Central Bank during 2007–2011 to follow a "green jersey agenda" in obfuscating the facts of Ireland's deteriorating banking system.[56][57][58][59] After the 2011–bailout by the EU–ECB–IMF (e.g. the European troika) of the Irish banking system, a number of non–Irish senior executives were placed in the Central Bank of Ireland, including the Board of the Bank. However, by 2017, almost all these non–Irish executives had departed the Central Bank, and some have publicised concerns about the Central Bank's tendency to push aside risk-management in pursuit of political and Government objectives.[60]

Mortgage controls post crisis[]

The Irish Celtic Tiger era was typified by large, interest-only mortgages, at high levels of loan-to-income values. After the 2011 bailout, the Central Bank introduced macro–prudential controls on mortgage lending both in terms of loan-to-value (a cap of 80% and 90% depending on circumstances), and loan-to-income (a cap of 3.5 times income).[40] A limited number of exemptions to these are available to Irish banks for both of these rules on an annual basis. Additionally, the Irish Government introduced a Help To Buy scheme, which allows first-time buyers to receive 5% of the cost price of a house as an income tax rebate – which loosened the LTI requirements further for eligible first-time buyers.[61] The Irish financial crisis showed the small and unusual nature of Ireland's economy (e.g. where a small number of U.S. corporates are 80% of Irish tax, 25% of Irish labour, 25 of top 50 Irish firms, and 57% of Irish value-add), led to foreign banks rapidly withdrawing capital from Ireland in times of stress.

Light-touch regulation[]

In 2017, it was shown that brochures of IFSC services firms market Ireland as a "light-touch" regulatory regime.[62][63][64][65][66][67][68] The Central Bank itself was paying rent to a US distressed debt-landlord who was using a Central Bank-regulated ICAV structure to avoid all Irish taxes.[69] In February 2018, the Central Bank expanded the little-used L–QIAIF vehicle to give the tax benefits as Section 110 SPVs but without requiring public accounts for the Irish CRO, which was how the abuses above were uncovered.[70] In June 2018, the Central Bank reported that distressed debt funds switched €55 billion, or 25% of Irish GNI*, out of Section 110 SPVs, and presumably into L–QIAIFs.[71] Such actions have been highlighted as those of a "captured state" by tax-experts.[72][73][74]

Distorted economic data[]

Research in June 2018 confirmed that Ireland, already a "major tax haven", was the world's largest tax haven.[76][77][78] In common with all tax havens, Ireland's economic data is distorted by the BEPS flows from tax management activities.[79][80] The top–10 GDP-per-capita countries, excluding natural resource countries, are all tax havens (see GDP-per-capita and tax havens).[81][82] This was shown dramatically in July 2016 during "leprechaun economics" affair when Apple re-structured its Double Irish BEPS tool, as agreed under an ongoing EU tax-investigation into Apple in Ireland, into a new Irish CAIA arrangement BEPS tool.

At this point, multinational profit shifting doesn't just distort Ireland's balance of payments; it constitutes Ireland’s balance of payments.

— Brad Setser and Cole Frank, Council on Foreign Relations, "Tax Avoidance and the Irish Balance of Payments", 25 April 2018[75]

Exaggerated credit cycles are a documented feature of tax havens as global capital markets misprice the "headline" debt-to-GDP in benign times, only to reprice aggressively in less benign times, leading to a credit crisis (discussed in tax haven credit cycles).[80] In 2017, the Central Bank of Ireland responded to this issue, post-leprehaun economics, by introducing Modified gross national income (or GNI*), as a more appropriate measure for Ireland's economy.[84][44]

Ireland has, more or less, stopped using GDP to measure its own economy. And on current trends [because Irish GDP is distorting EU–28 aggregate data], the eurozone taken as a whole may need to consider something similar.

The issues post-leprechaun economics, and "Modified GNI", are captured on page 34 of the OECD 2018 Ireland survey:[86]

- On a Gross Public Debt-to-GDP basis, Ireland's 2015 figure at 78.8% is not of concern;

- On a Gross Public Debt-to-GNI* basis, Ireland's 2015 figure at 116.5% is more serious, but not alarming;

- On a Gross Public Debt-Per-Capita basis, Ireland's 2015 figure at over $62,686 per capita, exceeds every other OECD country, except Japan.[87]

Commercial property bubbles[]

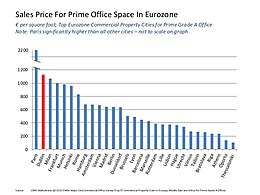

Ireland's status as a "major tax haven", and its exposure to a handful of major U.S. multinationals, mean that its commercial property market is prone to overinflating.[by whom?] This effect is amplified because the Irish State enables foreign investors to pay no taxes on Irish commercial property via the Central Bank regulated QIAIFs (and ICAVs in particular).[88][89] The ratio of the value of prime office in Dublin, to its cost-of-build, is the second-largest in the Eurozone, and only exceeded by Paris.[90][91] Irish office rents are close to London City office rents.[92]

Irish banks are the main lending institutions to Irish commercial property, and thus most exposed to material price distortions. As was seen in the Irish banking crisis, when global conditions weaken and the demand for Irish office space falls, the drop in Irish commercial valuations is more extreme than other markets. When this occurs in-sync with a global repricing of Irish credit, from a realisation of the level of artificial distortion in Irish economic data, the effects are further amplified. This risk was highlighted in 2014 when the Central Bank consulted the European Systemic Risk Board ("ESRB") after lobbying by IFSC tax-law firms to expand the L–QIAIF vehicle.[93] While the Central Bank agreed with the ESRB in 2014, it changed its mind in 2018, and decided to materially expand the L–QIAIFs vehicle (see § Light-touch regulation).

The longer-term risks of Irish commercial property were further increased with the U.S. Tax Cuts and Jobs Act of 2017, which fundamentally reduces the attractiveness of Ireland to U.S. multinationals, and could see Ireland lose its status as the major U.S. corporate tax haven.[94]

Control of total credit[]

Irish § Distorted economic data and the tendency to commercial and residential property bubbles has led to periods when Ireland's economy was over-leveraged and reliant on foreign capital. The ability of foreign capital to use Ireland's tax haven tools (IP–based BEPS tools, and Debt–based BEPS tools) to avoid Irish taxes, attracts further non-domestic credit. It has been shown that smaller countries with a high proportion of non–domestic capital are prone to severe credit cycles.[80] To resolve this imbalance in the 2007–2012 Irish financial crisis, Irish private-sector debt was transferred to Irish public-sector debt.[52][53] The result is that Ireland is now one of the EU–28's most leveraged countries on a private and public sector basis (when measured GNI or per-Capita measures, to limit the distortion by Irish GDP).[95][96][97][98] This means that the Irish State will not be able to bail out its banking system again for a considerable time.

During the 2008–2012 global credit crisis, reports showed Ireland's combined public and private sector credit as being the highest in the OECD (some reports[citation needed] added in IFSC SPV credit producing higher, but misleading, figures). In this regard, the Central Bank now tracks private and public credit in Ireland in its quarterly bulletins. Private credit is tracked on a credit-to-income ratio, while public sector credit is tracked on a debt-to-GNI* ratio.[99] In addition, as part of the post-crisis reforms, the independent statutory body, the Irish Fiscal Advisory Council, also reports on Irish leverage (public and private) and its sustainability.[100][101][102] It is still common to see other State bodies (e.g. NTMA and IDA Ireland) present the distorted, and misleading, Debt-to-GDP data in their reports.[citation needed]

See also[]

- Banknotes of the Republic of Ireland

- Coins of Ireland

- Economy of the Republic of Ireland

- European Central Bank

- Irish pound

- Irish modified GNI (or GNI star)

- Irish Fiscal Advisory Council

- Green Jersey Agenda

- Ireland as a tax haven

References[]

- ^ Jump up to: a b Weidner, Jan (2017). The Organisation and Structure of Central Banks (Thesis). Technische Universität Darmstadt.

- ^ "Central Bank Act, 1971". Irishstatutebook.ie. 28 July 1971. Retrieved 21 April 2012.

- ^ Previously the commercial Bank of Ireland, established in 1783, had been the government's banker.

- ^ "1980 – Central Bank of Ireland, Dame Street, Dublin". Archiseek. Archived from the original on 1 December 2010. Retrieved 10 April 2010.

- ^ "Central Bank of Ireland, Contact Us". Central Bank of Ireland. Retrieved 10 April 2017.

- ^ "Irish central bank sells old premises for €67 million". centralbanking.com. Central Banking Newsdesk. 17 January 2017. Retrieved 18 January 2017.

- ^ Honohan, Patrick (1994). Currency Board or Central Bank: Lessons from the Irish pound's link with Sterling 1928–79 (PDF). London: Centre for Economic Policy Research. p. 2.

- ^ "More euro in circulation than Irish pounds". RTÉ News. 11 January 2002. Retrieved 1 May 2007.

- ^ "Bank officials in 2006 said stress tests were not stressful enough". Irish Examiner. 12 February 2015.

- ^ "Central Bank aware of property bubble from 2004 – ex-employee". The Irish Times. 23 September 2015.

- ^ "Central Bank 'ignored my warnings' before economic crash – ESRI's FitzGerald". Breaking News.ie. 11 February 2015.

- ^ "Claim that Central Bank sought to gag economist on Northern Rock". The Sunday Business Post. 11 October 2015.

- ^ "Central Bank 'watered down' warnings of property bubble". The Irish Examiner. 11 June 2015.

- ^ "Joint Committee of Inquiry into the Banking Crisis. Witness Statement of Frank Browne" (PDF). Retrieved 24 September 2020.

- ^ Central Bank of Ireland- Financial Stability Report November 2007

- ^ "John Hurley: Last of the breed". Irish Independent. 3 October 2009. Retrieved 11 April 2010.

- ^ White, Dan (15 July 2009). "I'd rely on astrologer Fergus more than Central Bank chief". Evening Herald. Archived from the original on 4 September 2012. Retrieved 11 April 2010.

- ^ Keenan, Brendan (23 July 2009). "Fixing the Government is now more important than fixing our banks". Irish Independent. Retrieved 11 April 2010.

- ^ Curran, Richard (26 July 2009). "The inquisitor". Sunday Business Post. Retrieved 11 April 2010.[permanent dead link]

- ^ "Ahern admits to part in Irish crisis". Financial Times. 15 October 2009. Retrieved 11 April 2010.

- ^ "Admissions about lack of banking experience in regulator are shocking". The Irish Times. 11 June 2015.

- ^ "Continental shift". The Economist. 4 November 2010.

- ^ "Mad as hell at Ireland". The Irish Independent. 22 January 2011. Retrieved 21 April 2012.

- ^ "Our Approach to Authorisation". Archived from the original on 10 January 2011.

- ^ "How to start a bank in Ireland". Archived from the original on 4 June 2009.

- ^ McBride, Louise (1 April 2007). "Financial Regulator is questioned by own advisers". The Sunday Business Post. Retrieved 11 April 2010.[permanent dead link]

- ^ "Watchdog blasted in its own confidential report". The Irish Independent. 7 October 2009. Retrieved 21 April 2012.

- ^ Brian O’Mahony (8 October 2009). "Report exposes Financial Regulator's 'shortcomings'". Irish Examiner. Retrieved 21 April 2012.

- ^ "Wednesday Newspaper Review – Irish Business News and International Stories – – October 7, 2009". Finfacts.ie. Retrieved 21 April 2012.

- ^ "Report critical of Financial Regulator". The Irish Times. 14 October 2009. Retrieved 21 April 2012.

- ^ Murray, John (15 October 2009). "Ahern admits to part in Irish crisis". Financial Times. Retrieved 21 April 2012.

- ^ "Bertie Ahern: 'I don't consider myself a romantic person, maybe that was the problem'". The Irish Independent. 20 September 2009. Archived from the original on 3 August 2012. Retrieved 21 April 2012.

- ^ "Watchdog tells of shock at lax levels of enforcement – Irish, Business". The Irish Independent. 15 April 2010. Retrieved 21 April 2012.

- ^ "Regulator lacking top-level graduates". The Irish Independent. 18 April 2010. Retrieved 21 April 2012.

- ^ "Minister for Finance Brian Lenihan TD announces major reform of the institutional structures for regulation of financial services in Ireland". Press Releases. Department of Finance. 18 June 2009. Archived from the original on 19 July 2011. Retrieved 11 April 2010.

- ^ [1][dead link]

- ^ "Move to rules-based system will need a change in culture". Independent.ie. Retrieved 21 April 2012.

- ^ "I'd rely on astrologer Fergus more than Central Bank chief – Dan White, Columnists". Herald.ie. Archived from the original on 4 September 2012. Retrieved 21 April 2012.

- ^ "Ireland's biggest banks are getting a new regulator today and here's how it's going to work". thejournal.ie. 4 November 2014.

- ^ Jump up to: a b "What will the new Central Bank mortgage regime mean to you?". The Irish Times. 28 January 2015.

- ^ "Central Bank to review mortgage rules, says governor". The Irish Times. 8 January 2016. Retrieved 27 December 2018.

- ^ "REPORT OF THE ECONOMIC STATISTICS REVIEW GROUP" (PDF). Central Statistics Office. December 2016.

- ^ "ESRG Presentation and CSO Response" (PDF). Central Statistics Office. 4 February 2017.

- ^ Jump up to: a b "Leprechaun-proofing economic data". RTE News. 4 February 2017.

- ^ "Press Release - Central Bank of Ireland opens archives for public research". 1 August 2017.

- ^ "Central Bank Archive | Home page". archives.centralbank.ie. Retrieved 24 September 2020.

- ^ Paul, Mark. "Central Bank says average net wealth surges past €162,000 per person". The Irish Times. Retrieved 24 September 2020.

- ^ "Maurice O'Connell: Present Governor of Ireland's Central Bank". Moyvane.com. 1 January 2002. Archived from the original on 5 March 2010. Retrieved 11 April 2010.

- ^ Brennan, Joe. "New Central Bank governor faces bulging in-tray on first day". The Irish Times. Retrieved 2 September 2019.

- ^ "Dáil Éireann debate - Thursday, 23 Nov 2017". House of the Oireachtas. 23 November 2017.

Pearse Doherty: It was interesting that when [MEP] Matt Carthy put that to the Minister's predecessor (Michael Noonan), his response was that this was very unpatriotic and he should wear the green jersey. That was the former Minister's response to the fact there is a major loophole, whether intentional or unintentional, in our tax code that has allowed large companies to continue to use the double Irish [called single malt].

- ^ Jump up to: a b "Ireland : Lessons from Its Recovery from the Bank-Sovereign Loop". IMF. 23 October 2015.

- ^ Jump up to: a b "Irish government debt four times pre-crisis level, NTMA says". 10 July 2017.

- ^ Jump up to: a b "42% of Europe's banking crisis paid by Ireland". 16 January 2013.

- ^ "CSO paints a very different picture of Irish economy with new measure". Irish Times. 15 July 2017.

- ^ "New economic Leprechaun on loose as rate of growth plunges". Irish Independent. 15 July 2017.

- ^ "Irish banks were "pulling on the green jersey" during financial crisis, trial told". Courts News Ireland. 10 February 2016.

A former Anglo Irish Bank director has told the trial of four senior bankers accused of conspiring to mislead investors that there was a “green jersey agenda” which involved banks working together to help each other out during the financial turmoil of 2008.

- ^ "Ireland jails three top bankers over 2008 banking meltdown". Reuters. 29 July 2016.

Lawyers for the accused argued during the trial that their motivation in authorizing the deal was the “green jersey” agenda, the financial regulator’s request for Irish banks to support one another as the financial crisis worsened.

- ^ Judge ruled that it would not be right or practical to try to stop the Jury hearing about the "green jersey agenda"."Anglo verdict: Prosecution wanted 'green jersey' agenda removed". The Irish Times. 9 June 2016.

- ^ "The green jersey merchants haven't gone away". The Irish Times. 11 July 2016.

We heard a lot about the "green jersey" agenda during the Anglo trial, which finished during the week. It is the name given to the drive to protect the financial system as the crisis hit, taking in the government, Civil Service, regulators, banks and beyond.

- ^ "Former Regulator says Irish politicians mindless of IFSC risks in "green jersey" agenda". The Irish Times. 5 March 2018.

- ^ "Help to Buy (HTB) Part 15-04-46 Section 477C of the Taxes Consolidation Act (TCA) 1997" (PDF). Revenue Commission. 2017.

- ^ Professor Jim Stewart; Cillian Doyle (12 January 2017). "'Section 110' Companies: A Success story for Ireland" (PDF). Trinity College, Dublin.

- ^ "Ireland, Global Finance and the Russian Connection" (PDF). Professor Jim Stewart Cillian Doyle. 27 February 2018.

- ^ "How Russian Firms Funnelled €100bn through Dublin". The Sunday Business Post. 4 March 2018.

- ^ "More than €100bn in Russian Money funneled through Dublin". The Irish Times. 4 March 2018.

- ^ "A third of Ireland's shadow banking subject to little or no oversight". The Irish Times. 10 May 2017.

- ^ "Ireland is world's fourth-largest shadow banking hub". The Irish Times. 10 May 2017.

- ^ "IMF queries lawyers and bankers on hundreds of IFSC boards". The Irish Times. 30 September 2016.

- ^ "Central Bank landlord a vulture fund paying no Irish tax, says SF". The Irish Times. 28 August 2016.

- ^ "Central Bank of Ireland publishes notice of intention to amend the requirements for Loan Origination Qualifying Investor AIF" (PDF). Dillon Eustace Law Firm. February 2018.

- ^ "Tax-free funds once favoured by 'vultures' fall €55bn: Regulator attributes decline to the decision of funds to exit their so-called 'section 110 status'". The Irish Times. 28 June 2018.

- ^ "The capture of tax haven Ireland: "the bankers, hedge funds got virtually everything they wanted"". Nicholas Shaxson. May 2013.

- ^ "How Ireland became a tax haven and offshore financial centre". Nicholas Shaxson, Tax Justice Network. 11 November 2015.

The willingness to brush dirt under the carpet to support the financial sector, and an equating of these policies with patriotism (sometimes known in Ireland as the Green Jersey agenda,) contributed to the remarkable regulatory laxity with massive impacts in other nations (as well as in Ireland itself) as global financial firms sought an escape from financial regulation in Dublin.

- ^ Professor Philip Alston (13 February 2015). "'Nobody believes Ireland is not a tax haven' - UN official". Irish Times.

"The Irish authorities knew exactly what was going on, long before the international community finally blew the whistle.

- ^ Jump up to: a b "Tax Avoidance and the Irish Balance of Payments". Council on Foreign Relations. 25 April 2018.

- ^ Gabriel Zucman; Thomas Torslov; Ludvig Wier (June 2018). "The Missing Profits of Nations". National Bureau of Economic Research, Working Papers. p. 31.

Appendix Table 2: Tax Havens

- ^ "Zucman:Corporations Push Profits Into Corporate Tax Havens as Countries Struggle in Pursuit, Gabrial Zucman Study Says". Wall Street Journal. 10 June 2018.

Such profit shifting leads to a total annual revenue loss of $200 billion globally

- ^ "Ireland is the world's biggest corporate 'tax haven', say academics". Irish Times. 13 June 2018.

New Gabriel Zucman study claims State shelters more multinational profits than the entire Caribbean

- ^ Dhammika Dharmapala (2014). "What Do We Know About Base Erosion and Profit Shifting? A Review of the Empirical Literature". University of Chicago.

- ^ Jump up to: a b c Heike Joebges (January 2017). "CRISIS RECOVERY IN A COUNTRY WITH A HIGH PRESENCE OF FOREIGN-OWNED COMPANIES: The Case of Ireland" (PDF). IMK Macroeconomic Policy Institute, Hans-Böckler-Stiftung.

- ^ "How tax havens turn economic statistics into nonsense". Quartz. 11 June 2018.

- ^ "Piercing the Veil, FINANCE & DEVELOPMENT, JUNE 2018, VOL. 55, NO. 2". IMF Finance & Development. June 2018.

- ^ Seamus Coffey, Irish Fiscal Advisory Council (18 June 2018). "Who shifts profits to Ireland". Economic Incentives, University College Cork.

Eurostat’s structural business statistics give a range of measures of the business economy broken down by the controlling country of the enterprises. Here is the Gross Operating Surplus generated in Ireland in 2015 for the countries with figures reported by Eurostat.

- ^ "Report of the Economic Statistics Review Group". Central Statistics Office. 4 February 2017.

- ^ "Ireland Exports its Leprechaun". Council on Foreign Relations. 11 May 2018.

- ^ OECD Ireland Survey 2018 (PDF). OECD. March 2018. p. 34. ISBN 978-92-64-29177-5.

- ^ "National debt now €44000 per head". Irish Independent. 7 July 2017.

- ^ "Tax breaks for commercial property will fuel bubble". Irish Independent. 6 November 2016.

They'll do this by making commercial property investment, mainly by large foreign landlords, entirely tax-free. This will drive up commercial rents, suppress residential development, put Irish banks at risk, and deprive the State of much-needed funds.

- ^ "Finance Bill Could Turn Commercial Property Bubble into next Crash". Stephen Donnelly T.D. 6 November 2016.

- ^ "The commercial property bubble". Indymedia. 24 November 2016.

- ^ "Commercial office bubble rising". Stephen Donnelly. November 2016.

- ^ "Tax breaks for commercial property will fuel bubble". Irish Independent. 6 November 2016.

- ^ "Loan Origination QIAIFs-Central Bank Consults". Dillon Eustace Law Firm. 14 July 2014.

ESRB: Nonetheless, if not subject to adequate macro- and micro-prudential regulation, this activity could grow rapidly and introduce new sources of financial stability risk. It could also raise the financial system’s vulnerability to runs, contagion, excessive credit growth and pro-cyclicality.

- ^ Mihir A. Desai (26 December 2017). "Breaking Down the New U.S. Corporate Tax Law". Harvard Business Review.

So, if you think about a lot of technology companies that are housed in Ireland and have massive operations there, they’re not going to maybe need those in the same way, and those can be relocated back to the U.S.

- ^ "Who owes more money - the Irish or the Greeks?". The Irish Times. 4 June 2015.

- ^ "Why do the Irish still owe more than the Greeks?". The Irish Times. 7 March 2017.

- ^ "Ireland's colossal level of indebtedness leaves any new government with precious little room for manoeuvre". Irish Independent. 16 April 2016.

- ^ "Net National debt now €44000 per head, 2nd highest in the World". Irish Independent. 7 July 2017.

- ^ "Quarterly Statistical Release November 2017" (PDF). Central Bank of Ireland. November 2017.

- ^ "Debt levels remain high following the crisis June FAR Slide 7" (PDF). Irish Fiscal Advisory Council. June 2017.

- ^ "Section 1.2.2 Recent Fiscal Context June FAR Page 14" (PDF). Irish Fiscal Advisory Council. June 2017.

- ^ "Future Implications of the Debt Rule" (PDF). Irish Fiscal Advisory Council. June 2014.

External links[]

Media related to Central Bank of Ireland at Wikimedia Commons

Media related to Central Bank of Ireland at Wikimedia Commons- Official website

- Central Bank of Ireland on Twitter

Coordinates: 53°20′52″N 6°14′05″W / 53.34765°N 6.23464°W

| show Authority control |

|---|

- Central Bank of Ireland

- Regulation in Ireland

- Government agencies of the Republic of Ireland

- European System of Central Banks

- Banks of Ireland

- Banks established in 1943

- Central banks

- Financial regulatory authorities

- 1943 establishments in Ireland

- Dublin Docklands