Free market

| Part of a series on |

| Economic systems |

|---|

|

| Part of a series on |

| Liberalism |

|---|

|

|

In economics, a free market is a system in which the prices for goods and services are self-regulated by buyers and sellers negotiating in an open market. In a free market, the laws and forces of supply and demand are free from any intervention by a government or other authority, and from all forms of economic privilege, monopolies and artificial scarcities.[1] Proponents of the concept of free market contrast it with a regulated market in which a government intervenes in supply and demand through various methods such as tariffs used to restrict trade and to protect the local economy. In an idealized free-market economy, also called a liberal market economy, prices for goods and services are set freely by the forces of supply and demand and are allowed to reach their point of equilibrium without intervention by government policy.

Scholars contrast the concept of a free market with the concept of a coordinated market in fields of study such as political economy, new institutional economics, economic sociology and political science. All of these fields emphasize the importance in currently existing market systems of rule-making institutions external to the simple forces of supply and demand which create space for those forces to operate to control productive output and distribution. Although free markets are commonly associated with capitalism in contemporary usage and popular culture, free markets have also been components in some forms of socialism.[2]

Criticism of the theoretical concept may regard systems with significant market power, inequality of bargaining power, or information asymmetry as less than free, with regulation being necessary to control those imbalances in order to allow markets to function more efficiently as well as produce more desirable social outcomes.

Economic systems[]

Capitalism[]

| Part of a series on |

| Capitalism |

|---|

|

Capitalism is an economic system based on the private ownership of the means of production and their operation for profit.[3][4][5][6] Central characteristics of capitalism include capital accumulation, competitive markets, a price system, private property and the recognition of property rights, voluntary exchange and wage labor.[7][8] In a capitalist market economy, decision-making and investments are determined by every owner of wealth, property or production ability in capital and financial markets whereas prices and the distribution of goods and services are mainly determined by competition in goods and services markets.[9]

Economists, historians, political economists and sociologists have adopted different perspectives in their analyses of capitalism and have recognized various forms of it in practice. These include laissez-faire or free-market capitalism, state capitalism and welfare capitalism. Different forms of capitalism feature varying degrees of free markets, public ownership,[10] obstacles to free competition and state-sanctioned social policies. The degree of competition in markets and the role of intervention and regulation as well as the scope of state ownership vary across different models of capitalism.[11][12] The extent to which different markets are free and the rules defining private property are matters of politics and policy. Most of the existing capitalist economies are mixed economies that combine elements of free markets with state intervention and in some cases economic planning.[13]

Market economies have existed under many forms of government and in many different times, places and cultures. Modern capitalist societies—marked by a universalization of money-based social relations, a consistently large and system-wide class of workers who must work for wages (the proletariat) and a capitalist class which owns the means of production—developed in Western Europe in a process that led to the Industrial Revolution. Capitalist systems with varying degrees of direct government intervention have since become dominant in the Western world and continue to spread. Capitalism has been shown to be strongly correlated with economic growth.[14]

Critics of capitalism argue that it concentrates power in the hands of a minority capitalist class that exists through the exploitation of the majority working class and their labor, prioritizes profit over social good, natural resources and the environment, is an engine of inequality, corruption and economic instabilities, and that many are not able to access its purported benefits and freedoms, such as freely investing. Supporters argue that it provides better products and innovation through competition, promotes pluralism and decentralization of power, disperses wealth to people who are able to invest in useful enterprises based on market demands, allows for a flexible incentive system where efficiency and sustainability are priorities to protect capital, creates strong economic growth and yields productivity and prosperity that greatly benefit society.

Georgism[]

For classical economists such as Adam Smith, the term free market does not necessarily refer to a market free from government interference, but rather free from all forms of economic privilege, monopolies and artificial scarcities.[1] This implies that economic rents, i.e. profits generated from a lack of perfect competition, must be reduced or eliminated as much as possible through free competition.

Economic theory suggests the returns to land and other natural resources are economic rents that cannot be reduced in such a way because of their perfect inelastic supply.[15] Some economic thinkers emphasize the need to share those rents as an essential requirement for a well functioning market. It is suggested this would both eliminate the need for regular taxes that have a negative effect on trade (see deadweight loss) as well as release land and resources that are speculated upon or monopolised. Two features that improve the competition and free market mechanisms. Winston Churchill supported this view by the following statement: "Land is the mother of all monopoly".[16] The American economist and social philosopher Henry George, the most famous proponent of this thesis, wanted to accomplish this through a high land value tax that replaces all other taxes.[17] Followers of his ideas are often called Georgists or geoists and geolibertarians.

Léon Walras, one of the founders of the neoclassical economics who helped formulate the general equilibrium theory, had a very similar view. He argued that free competition could only be realized under conditions of state ownership of natural resources and land. Additionally, income taxes could be eliminated because the state would receive income to finance public services through owning such resources and enterprises.[18]

Laissez-faire[]

The laissez-faire principle expresses a preference for an absence of non-market pressures on prices and wages such as those from discriminatory government taxes, subsidies, tariffs, regulations of purely private behavior, or government-granted or coercive monopolies. In The Pure Theory of Capital, Friedrich Hayek argued that the goal is the preservation of the unique information contained in the price itself.[19]

The definition of free market has been disputed and made complex by collectivist political philosophers and socialist economic ideas.[1] This contention arose from the divergence from classical economists such as Richard Cantillon, Adam Smith, David Ricardo and Thomas Robert Malthus and from the continental economics developed primarily by the Spanish scholastic and French classical economists, including Anne-Robert-Jacques Turgot, Baron de Laune, Jean-Baptiste Say and Frédéric Bastiat. During the marginal revolution, subjective value theory was rediscovered.[20]

Although laissez-faire has been commonly associated with capitalism, there is a similar economic theory associated with socialism called left-wing or socialist laissez-faire, also known as free-market anarchism, free-market anti-capitalism and free-market socialism to distinguish it from laissez-faire capitalism.[21][22][23] Critics of laissez-faire as commonly understood argue that a truly laissez-faire system would be anti-capitalist and socialist.[24][25] American individualist anarchists such as Benjamin Tucker saw themselves as economic free-market socialists and political individualists while arguing that their "anarchistic socialism" or "individual anarchism" was "consistent Manchesterism".[26]

Socialism[]

Various forms of socialism based on free markets have existed since the 19th century. Early notable socialist proponents of free markets include Pierre-Joseph Proudhon, Benjamin Tucker and the Ricardian socialists. These economists believed that genuinely free markets and voluntary exchange could not exist within the exploitative conditions of capitalism. These proposals ranged from various forms of worker cooperatives operating in a free-market economy such as the mutualist system proposed by Proudhon, to state-owned enterprises operating in unregulated and open markets. These models of socialism are not to be confused with other forms of market socialism (e.g. the Lange model) where publicly owned enterprises are coordinated by various degrees of economic planning, or where capital good prices are determined through marginal cost pricing.

Advocates of free-market socialism such as Jaroslav Vanek argue that genuinely free markets are not possible under conditions of private ownership of productive property. Instead, he contends that the class differences and inequalities in income and power that result from private ownership enable the interests of the dominant class to skew the market to their favor, either in the form of monopoly and market power, or by utilizing their wealth and resources to legislate government policies that benefit their specific business interests. Additionally, Vanek states that workers in a socialist economy based on cooperative and self-managed enterprises have stronger incentives to maximize productivity because they would receive a share of the profits (based on the overall performance of their enterprise) in addition to receiving their fixed wage or salary. The stronger incentives to maximize productivity that he conceives as possible in a socialist economy based on cooperative and self-managed enterprises might be accomplished in a free-market economy if employee-owned companies were the norm as envisioned by various thinkers including Louis O. Kelso and James S. Albus.[27]

Socialists also assert that free-market capitalism leads to an excessively skewed distributions of income and economic instabilities which in turn leads to social instability. Corrective measures in the form of social welfare, re-distributive taxation and regulatory measures and their associated administrative costs which are required create agency costs for society. These costs would not be required in a self-managed socialist economy.[28]

Concepts[]

Economic equilibrium[]

With varying degrees of mathematical rigor over time, the general equilibrium theory has demonstrated that under certain conditions of competition the law of supply and demand predominates in this ideal free and competitive market, influencing prices toward an equilibrium that balances the demands for the products against the supplies.[29] At these equilibrium prices, the market distributes the products to the purchasers according to each purchaser's preference or utility for each product and within the relative limits of each buyer's purchasing power. This result is described as market efficiency, or more specifically a Pareto optimum.

This equilibrating behavior of free markets requires certain assumptions about their agents—collectively known as perfect competition—which therefore cannot be results of the market that they create. Among these assumptions are several which are impossible to fully achieve in a real market, such as complete information, interchangeable goods and services and lack of market power. The question then is what approximations of these conditions guarantee approximations of market efficiency and which failures in competition generate overall market failures. Several Nobel Prizes in Economics have been awarded for analyses of market failures due to asymmetric information.

Low barriers to entry[]

A free market does not require the existence of competition, however, it does require a framework that allows new market entrants. Hence, in the lack of coercive barriers, for example, paid licensing certification for certain services and businesses, competition between businesses flourishes all through the demands of consumers, or buyers. It often suggests the presence of the profit motive, although neither a profit motive or profit itself are necessary for a free market.[citation needed] All modern free markets are understood to include entrepreneurs, both individuals and businesses. Typically, a modern free-market economy would include other features such as a stock exchange and a financial services sector, but they do not define it.

Perfect competition and market failure[]

Conditions that must exist for unregulated markets to behave as free markets are summarized at perfect competition. An absence of any of these perfect competition ideal conditions is a market failure. Most schools of economics[which?] allow that regulatory intervention may provide a substitute force to counter a market failure. Under this thinking, this form of market regulation may be better than an unregulated market at providing a free market.

Spontaneous order[]

Friedrich Hayek popularized the view that market economies promote spontaneous order which results in a better "allocation of societal resources than any design could achieve".[30] According to this view, market economies are characterized by the formation of complex transactional networks that produce and distribute goods and services throughout the economy. These networks are not designed, but they nevertheless emerge as a result of decentralized individual economic decisions. The idea of spontaneous order is an elaboration on the invisible hand proposed by Adam Smith in The Wealth of Nations. About the individual, Smith wrote:

By preferring the support of domestic to that of foreign industry, he intends only his own security; and by directing that industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention. Nor is it always the worse for society that it was no part of it. By pursuing his own interest, he frequently promotes that of the society more effectually than when he really intends to promote it. I have never known much good done by those who affected to trade for the public good.[31]

Smith pointed out that one does not get one's dinner by appealing to the brother-love of the butcher, the farmer or the baker. Rather, one appeals to their self-interest and pays them for their labor, arguing:

It is not from the benevolence of the butcher, the brewer or the baker, that we expect our dinner, but from their regard to their own self-interest. We address ourselves, not to their humanity but to their self-love, and never talk to them of our own necessities but of their advantages.[32]

Supporters of this view claim that spontaneous order is superior to any order that does not allow individuals to make their own choices of what to produce, what to buy, what to sell and at what prices due to the number and complexity of the factors involved. They further believe that any attempt to implement central planning will result in more disorder, or a less efficient production and distribution of goods and services.

Critics such as political economist Karl Polanyi question whether a spontaneously ordered market can exist, completely free of distortions of political policy, claiming that even the ostensibly freest markets require a state to exercise coercive power in some areas, namely to enforce contracts, govern the formation of labor unions, spell out the rights and obligations of corporations, shape who has standing to bring legal actions and define what constitutes an unacceptable conflict of interest.[33]

Supply and demand[]

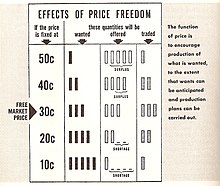

Demand for an item (such as goods or services) refers to the economic market pressure from people trying to buy it. Buyers have a maximum price they are willing to pay and sellers have a minimum price they are willing to offer their product. The point at which the supply and demand curves meet is the equilibrium price of the good and quantity demanded. Sellers willing to offer their goods at a lower price than the equilibrium price receive the difference as producer surplus. Buyers willing to pay for goods at a higher price than the equilibrium price receive the difference as consumer surplus.[34]

The model is commonly applied to wages in the market for labor. The typical roles of supplier and consumer are reversed. The suppliers are individuals, who try to sell (supply) their labor for the highest price. The consumers are businesses, which try to buy (demand) the type of labor they need at the lowest price. As more people offer their labor in that market, the equilibrium wage decreases and the equilibrium level of employment increases as the supply curve shifts to the right. The opposite happens if fewer people offer their wages in the market as the supply curve shifts to the left.[34]

In a free market, individuals and firms taking part in these transactions have the liberty to enter, leave and participate in the market as they so choose. Prices and quantities are allowed to adjust according to economic conditions in order to reach equilibrium and properly allocate resources. However, in many countries around the world governments seek to intervene in the free market in order to achieve certain social or political agendas.[35] Governments may attempt to create social equality or equality of outcome by intervening in the market through actions such as imposing a minimum wage (price floor) or erecting price controls (price ceiling). Other lesser-known goals are also pursued, such as in the United States, where the federal government subsidizes owners of fertile land to not grow crops in order to prevent the supply curve from further shifting to the right and decreasing the equilibrium price. This is done under the justification of maintaining farmers' profits; due to the relative inelasticity of demand for crops, increased supply would lower the price but not significantly increase quantity demanded, thus placing pressure on farmers to exit the market.[36] Those interventions are often done in the name of maintaining basic assumptions of free markets such as the idea that the costs of production must be included in the price of goods. Pollution and depletion costs are sometimes not included in the cost of production (a manufacturer that withdraws water at one location then discharges it polluted downstream, avoiding the cost of treating the water), therefore governments may opt to impose regulations in an attempt to try to internalize all of the cost of production and ultimately include them in the price of the goods.

Advocates of the free market contend that government intervention hampers economic growth by disrupting the natural allocation of resources according to supply and demand while critics of the free market contend that government intervention is sometimes necessary to protect a country's economy from better-developed and more influential economies, while providing the stability necessary for wise long-term investment. Milton Friedman pointed to failures of central planning, price controls and state-owned corporations, particularly in the Soviet Union and China[37] while Ha-Joon Chang cites the examples of post-war Japan and the growth of South Korea's steel industry.[38]

Criticism[]

Critics of the free market have argued that in real world situations it has proven to be susceptible to the development of price fixing monopolies.[39] Such reasoning has led to government intervention, e.g. the United States antitrust law.

Two prominent Canadian authors argue that government at times has to intervene to ensure competition in large and important industries. Naomi Klein illustrates this roughly in her work The Shock Doctrine and John Ralston Saul more humorously illustrates this through various examples in The Collapse of Globalism and the Reinvention of the World.[40] While its supporters argue that only a free market can create healthy competition and therefore more business and reasonable prices, opponents say that a free market in its purest form may result in the opposite. According to Klein and Ralston, the merging of companies into giant corporations or the privatization of government-run industry and national assets often result in monopolies or oligopolies requiring government intervention to force competition and reasonable prices.[40] Another form of market failure is speculation, where transactions are made to profit from short term fluctuation, rather from the intrinsic value of the companies or products. This criticism has been challenged by historians such as Lawrence Reed, who argued that monopolies have historically failed to form even in the absence of antitrust law.[41] This is because monopolies are inherently difficult to maintain as a company that tries to maintain its monopoly by buying out new competitors, for instance, is incentivizing newcomers to enter the market in hope of a buy-out.

American philosopher and author Cornel West has derisively termed what he perceives as dogmatic arguments for laissez-faire economic policies as free-market fundamentalism. West has contended that such mentality "trivializes the concern for public interest" and "makes money-driven, poll-obsessed elected officials deferential to corporate goals of profit – often at the cost of the common good".[42] American political philosopher Michael J. Sandel contends that in the last thirty years the United States has moved beyond just having a market economy and has become a market society where literally everything is for sale, including aspects of social and civic life such as education, access to justice and political influence.[43] The economic historian Karl Polanyi was highly critical of the idea of the market-based society in his book The Great Transformation, noting that any attempt at its creation would undermine human society and the common good.[44]

Critics of free market economics range from those who reject markets entirely in favour of a planned economy as advocated by various Marxists to those who wish to see market failures regulated to various degrees or supplemented by government interventions. Keynesians support market roles for government such as using fiscal policy for economic stimulus when actions in the private sector lead to sub-optimal economic outcomes of depressions or recessions. Business cycle is used by Keynesians to explain liquidity traps, by which underconsumption occurs, to argue for government intervention with fiscal policy. David McNally of the University of Houston argues in the Marxist tradition that the logic of the market inherently produces inequitable outcomes and leads to unequal exchanges, arguing that Adam Smith's moral intent and moral philosophy espousing equal exchange was undermined by the practice of the free market he championed. According to McNally, the development of the market economy involved coercion, exploitation and violence that Smith's moral philosophy could not countenance. McNally also criticizes market socialists for believing in the possibility of fair markets based on equal exchanges to be achieved by purging parasitical elements from the market economy such as private ownership of the means of production, arguing that market socialism is an oxymoron when socialism is defined as an end to wage labour.[45]

Some would argue that only one known example of a true free market exists, namely the black market. The black market is under constant threat by the police, but under no circumstances do the police regulate the substances that are being created. The black market produces wholly unregulated goods and are purchased and consumed unregulated. That is to say, anyone can produce anything at any time and anyone can purchase anything available at any time. The alternative view is that the black market is not a free market at all since high prices and natural monopolies are often enforced through murder, theft and destruction. Black markets can only exist peripheral to regulated markets where laws are being regularly enforced.[citation needed]

See also[]

- Binary economics

- Crony capitalism

- Economic liberalism

- Freedom of choice

- Free price system

- Grey market

- Left-wing market anarchism

- Market economy

- Neoliberalism

- Participatory economics

- Quasi-market

- Self-managed economy

- Transparency (market)

Notes[]

- ^ Jump up to: a b c Popper, Karl (1994). The Open Society and Its Enemies. Routledge Classics. ISBN 978-0-415-61021-6.

- ^ Bockman, Johanna (2011). Markets in the name of Socialism: The Left-Wing origins of Neoliberalism. Stanford University Press. ISBN 978-0-8047-7566-3.

- ^ Zimbalist, Sherman and Brown, Andrew, Howard J. and Stuart (October 1988). Comparing Economic Systems: A Political-Economic Approach. Harcourt College Pub. pp. 6–7. ISBN 978-0-15-512403-5.

Pure capitalism is defined as a system wherein all of the means of production (physical capital) are privately owned and run by the capitalist class for a profit, while most other people are workers who work for a salary or wage (and who do not own the capital or the product).

- ^ Rosser, Mariana V.; Rosser, J Barkley (23 July 2003). Comparative Economics in a Transforming World Economy. MIT Press. p. 7. ISBN 978-0-262-18234-8.

In capitalist economies, land and produced means of production (the capital stock) are owned by private individuals or groups of private individuals organized as firms.

- ^ Chris Jenks. Core Sociological Dichotomies. "Capitalism, as a mode of production, is an economic system of manufacture and exchange which is geared toward the production and sale of commodities within a market for profit, where the manufacture of commodities consists of the use of the formally free labor of workers in exchange for a wage to create commodities in which the manufacturer extracts surplus value from the labor of the workers in terms of the difference between the wages paid to the worker and the value of the commodity produced by him/her to generate that profit." London; Thousand Oaks, CA; New Delhi. Sage. p. 383.

- ^ Gilpin, Robert (5 June 2018). The Challenge of Global Capitalism : The World Economy in the 21st Century. ISBN 9780691186474. OCLC 1076397003.

- ^ Heilbroner, Robert L. "Capitalism" Archived 28 October 2017 at the Wayback Machine. Steven N. Durlauf and Lawrence E. Blume, eds. The New Palgrave Dictionary of Economics. 2nd ed. (Palgrave Macmillan, 2008) doi:10.1057/9780230226203.0198.

- ^ Louis Hyman and Edward E. Baptist (2014). American Capitalism: A Reader Archived 22 May 2015 at the Wayback Machine. Simon & Schuster. ISBN 978-1-4767-8431-1.

- ^ Gregory, Paul; Stuart, Robert (2013). The Global Economy and its Economic Systems. South-Western College Pub. p. 41. ISBN 978-1-285-05535-0.

Capitalism is characterized by private ownership of the factors of production. Decision making is decentralized and rests with the owners of the factors of production. Their decision making is coordinated by the market, which provides the necessary information. Material incentives are used to motivate participants.

- ^ Gregory and Stuart, Paul and Robert (28 February 2013). The Global Economy and its Economic Systems. South-Western College Pub. p. 107. ISBN 978-1-285-05535-0.

Real-world capitalist systems are mixed, some having higher shares of public ownership than others. The mix changes when privatization or nationalization occurs. Privatization is when property that had been state-owned is transferred to private owners. Nationalization occurs when privately owned property becomes publicly owned.

- ^ Macmillan Dictionary of Modern Economics, 3rd Ed., 1986, p. 54.

- ^ Bronk, Richard (Summer 2000). "Which model of capitalism?". OECD Observer. Vol. 1999 no. 221–22. OECD. pp. 12–15. Archived from the original on 6 April 2018. Retrieved 6 April 2018.

- ^ Stilwell, Frank. "Political Economy: the Contest of Economic Ideas". First Edition. Oxford University Press. Melbourne, Australia. 2002.

- ^ Sy, Wilson N. (18 September 2016). "Capitalism and Economic Growth Across the World". Rochester, NY. SSRN 2840425.

For 40 largest countries in the International Monetary Fund (IMF) database, it is shown statistically that capitalism, between 2003 and 2012, is positively correlated significantly to economic growth.

Cite journal requires|journal=(help) - ^ Adam Smith, The Wealth of Nations Book V, Chapter 2, Part 2, Article I: Taxes upon the Rent of Houses.

- ^ House Of Commons May 4th; King's Theatre, Edinburgh, July 17

- ^ Backhaus, "Henry George's Ingenious Tax," pp. 453–58.

- ^ Bockman, Johanna (2011). Markets in the name of Socialism: The Left-Wing origins of Neoliberalism. Stanford University Press. p. 21. ISBN 978-0-8047-7566-3.

For Walras, socialism would provide the necessary institutions for free competition and social justice. Socialism, in Walras's view, entailed state ownership of land and natural resources and the abolition of income taxes. As owner of land and natural resources, the state could then lease these resources to many individuals and groups which would eliminate monopolies and thus enable free competition. The leasing of land and natural resources would also provide enough state revenue to make income taxes unnecessary, allowing a worker to invest his savings and become 'an owner or capitalist at the same time that he remains a worker.

- ^ Hayek, Friedrich (1941). The Pure Theory of Capital.

- ^ Popper, Karl (2002). The Poverty of Historicism. Routledge Classics. ISBN 0415278465.

- ^ Chartier, Gary; Johnson, Charles W. (2011). Markets Not Capitalism: Individualist Anarchism Against Bosses, Inequality, Corporate Power, and Structural Poverty. Brooklyn, NY:Minor Compositions/Autonomedia

- ^ "It introduces an eye-opening approach to radical social thought, rooted equally in libertarian socialism and market anarchism." Chartier, Gary; Johnson, Charles W. (2011). Markets Not Capitalism: Individualist Anarchism Against Bosses, Inequality, Corporate Power, and Structural Poverty. Brooklyn, NY: Minor Compositions/Autonomedia. p. back cover.

- ^ "But there has always been a market-oriented strand of libertarian socialism that emphasizes voluntary cooperation between producers. And markets, properly understood, have always been about cooperation. As a commenter at Reason magazine's Hit&Run blog, remarking on Jesse Walker's link to the Kelly article, put it: "every trade is a cooperative act." In fact, it's a fairly common observation among market anarchists that genuinely free markets have the most legitimate claim to the label "socialism." "Socialism: A Perfectly Good Word Rehabilitated" by Kevin Carson at website of Center for a Stateless Society.

- ^ Nick Manley, "Brief Introduction To Left-Wing Laissez Faire Economic Theory: Part One".

- ^ Nick Manley, "Brief Introduction To Left-Wing Laissez Faire Economic Theory: Part Two".

- ^ Tucker, Benjamin (1926). Individual Liberty: Selections from the Writings of Benjamin R. Tucker. New York: Vanguard Press. pp. 1–19.

- ^ "Cooperative Economics: An Interview with Jaroslav Vanek". Interview by Albert Perkins. Retrieved March 17, 2011.

- ^ The Political Economy of Socialism, by Horvat, Branko (1982), pp. 197–98.

- ^ Theory of Value by Gérard Debreu.

- ^ Hayek cited. Petsoulas, Christina. Hayek's Liberalism and Its Origins: His Idea of Spontaneous Order and the Scottish Enlightenment. Routledge. 2001. p. 2.

- ^ Smith, Adam (1827). The Wealth of Nations. Book IV. p. 184.

- ^ Smith, Adam (1776). "2". The Wealth of Nations. 1. London: W. Strahan and T. Cadell.

- ^ Hacker, Jacob S.; Pierson, Paul (2010). Winner-Take-All Politics: How Washington Made the Rich Richer – and Turned Its Back on the Middle Class. Simon & Schuster. p. 55.

- ^ Jump up to: a b Judd, K. L. (1997). "Computational economics and economic theory: Substitutes or complements?" (PDF). Journal of Economic Dynamics and Control. 21 (6): 907–42. doi:10.1016/S0165-1889(97)00010-9. S2CID 55347101.

- ^ "Archived copy". Archived from the original on 2014-05-22. Retrieved 2014-06-06.CS1 maint: archived copy as title (link)

- ^ "Farm Program Pays $1.3 Billion to People Who Don't Farm". Washington Post. 2 July 2006. Retrieved 3 June 2014.

- ^ Ip, Greg and Mark Whitehouse, "How Milton Friedman Changed Economics, Policy and Markets", Wall Street Journal Online (November 17, 2006).

- ^ "Bad Samaritans: The Myth of Free Trade and the Secret History of Capitalism", Ha-Joon Chang, Bloomsbury Press, ISBN 978-1596915985

- ^ Tarbell, Ida (1904). The History of the Standard Oil Company. McClure, Phillips and Co.

- ^ Jump up to: a b Saul, John The End of Globalism.

- ^ "Cliche #41: "Rockefeller’s Standard Oil Company Proved That We Needed Anti-Trust Laws to Fight Such Market Monopolies", The Freeman, January 23, 2015. Retrieved December 20, 2016.

- ^ "Cornel West: Democracy Matters", The Globalist, January 24, 2005. Retrieved October 9, 2014.

- ^ Michael J. Sandel (June 2013). Why we shouldn't trust markets with our civic life. TED. Retrieved January 11, 2015.

- ^ Henry Farrell (July 18, 2014). The free market is an impossible utopia. The Washington Post. Retrieved January 11, 2015.

- ^ McNally, David (1993). Against the Market: Political Economy, Market Socialism and the Marxist Critique. Verso. ISBN 978-0-86091-606-2.

Further reading[]

- Block, Fred and Somers, Margaret R (2014). The Power of Market Fundamentalism: Karl Polanyi's Critique. Harvard University Press. ISBN 0674050711.

- Boettke, Peter J. "What Went Wrong with Economics?", Critical Review Vol. 11, No. 1, pp. 35, 58.

- Harcourt, Bernard (2012). The Illusion of Free Markets: Punishment and the Myth of Natural Order. Harvard University Press. ISBN 0674066162.

- Cox, Harvey (2016). The Market as God. Harvard University Press. ISBN 9780674659681.

- Hayek, Friedrich A. (1948). Individualism and Economic Order. Chicago: University of Chicago Press. vii, 271, [1].

- Palda, Filip (2011) Pareto's Republic and the New Science of Peace 2011 [1] chapters online. Published by Cooper-Wolfling. ISBN 978-0-9877880-0-9.

- Sandel, Michael J. (2013). What Money Can't Buy: The Moral Limits of Markets. Farrar, Straus and Giroux. ISBN 0374533652.

- Stiglitz, Joseph. (1994). Whither Socialism? Cambridge, Massachusetts: MIT Press.

- Verhaeghe, Paul (2014). What About Me? The Struggle for Identity in a Market-Based Society. Scribe Publications. ISBN 1922247375.

- Robert Kuttner, "The Man from Red Vienna" (review of Gareth Dale, Karl Polanyi: A Life on the Left, Columbia University Press, 381 pp.), The New York Review of Books, vol. LXIV, no. 20 (21 December 2017), pp. 55–57. "In sum, Polanyi got some details wrong, but he got the big picture right. Democracy cannot survive an excessively free market; and containing the market is the task of politics. To ignore that is to court fascism." (Robert Kuttner, p. 57).

External links[]

| Wikiquote has quotations related to: Free market |

- "Free market" at Encyclopædia Britannica

- "Free Enterprise: The Economics of Cooperation" looks at how communication, coordination and cooperation interact to make free markets work

| show Age of Enlightenment |

|---|

| show Authority control |

|---|

- Free market

- Anarchism

- Capitalism

- Classical liberalism

- Economic ideologies

- Economic liberalism

- Economic systems

- Georgism

- Libertarianism

- Libertarian theory

- Market (economics)

- Market socialism

- Socialism